The Memory Card Company That Became Wall Street's Biggest AI Surprise

How SanDisk went from selling SD cards to becoming 2025's best-performing stock

SanDisk stock surged 559% in 2025, making it the best-performing stock in the S&P 500, on the back of what industry executives are calling the worst memory shortage in a decade. On January 6, 2026 alone, shares jumped 27% after NVIDIA CEO Jensen Huang declared at CES that AI storage will become “the largest storage market in the world.”

The company that three immigrant entrepreneurs founded in 1988 to make “digital film” for cameras that didn’t yet exist has transformed into the beating heart of AI infrastructure.

Here’s how a company that nearly died multiple times became one of the biggest winners of the AI revolution—and what founders can learn from their 38-year journey.

Part One: The Crisis Nobody Saw Coming

On January 6, 2026, NVIDIA CEO Jensen Huang took the stage at CES and fundamentally reframed how the world thinks about storage.

“AI data storage is a completely unserved market today,” Huang declared. “This market will likely be the largest storage market in the world, basically holding the working memory of the world’s AIs.”

The market’s response was immediate. SanDisk shares rocketed 27% that day, the stock’s second-largest single-day gain ever, pushing the market cap to $51 billion. Western Digital, which still owns 20% of SanDisk following their February 2025 spin-off, surged 17% to an all-time high.

What made this moment different wasn’t just demand. It was the structural shift in how AI systems need storage.

NVIDIA’s new rack design requires up to 17 terabytes of flash storage per unit. At projected volumes, NVIDIA alone will consume nearly 0.1% of the entire global supply. One customer. One product line.

Flash prices increased 33-38% in one quarter. The drives in your laptop jumped 40%. SanDisk’s enterprise products doubled in price since November, with another 50% increase planned. Memory makers have inventory lasting only until March. Some expect to run completely out of stock.

Phison CEO Khein-Seng Pua delivered the most sobering assessment:

“Every NAND manufacturer is sold out for 2026. This shortage could last 10 years.”

Why? Because nobody’s building new factories. A flash memory fab costs $10-20 billion and takes years to construct. After the brutal 2023 collapse when industry revenue fell 66%, nobody wants to be caught with excess capacity when the cycle turns.

The only new capacity coming online through 2027 is one facility in Japan. While Micron broke ground on a new 'megafab' in New York yesterday, their own press release confirmed production won't start until 2030. That leaves a four-year air pocket where demand explodes and supply is fixed.

Meanwhile, Amazon, Google, Microsoft, and Meta are buying everything available at any price.

This is the environment that made a memory card company the best-performing stock in the S&P 500.

Part Two: The $19 Billion Divorce

To understand how SanDisk captured this moment, you need to understand what happened on February 24, 2025.

That’s the day SanDisk started trading independently after nine years buried inside Western Digital, the hard drive company that acquired them for $16 billion in 2016. When the two companies separated, investors valued the newly independent SanDisk at $19 billion. Western Digital distributed 80% of SanDisk shares to shareholders and kept 20% to sell later.

But here’s what mattered most: the CEO had to choose which company to lead.

David Goeckeler was 63 years old, a former Cisco executive who’d spent decades in enterprise technology. As CEO of Western Digital, he faced an impossible choice. Stay with the stable, predictable hard drive business that had been slowly declining for years. Or bet everything on flash memory and AI infrastructure.

He chose SanDisk.

That choice signaled where the smart money was going. The timing turned out to be either brilliant or lucky, probably both. The spin-off completed just as AI memory demand was exploding. SanDisk was suddenly free to focus entirely on flash while Western Digital managed the slow decline of spinning disks.

The market validated the choice spectacularly.

Then vs. Now:

February 2025: Stock starts trading at $38

January 2026: Stock hits $330 (768% appreciation in 10 months)

Nine months after independence: Added to S&P 500

Revenue Transformation:

Before: 70% from consumer products, 30% from enterprise

After: 55% from enterprise data centers, 15% from consumer products

This wasn’t just shifting numbers on a spreadsheet. The business model had fundamentally flipped. SanDisk used to make money selling memory cards to consumers at Best Buy, competing mostly on price with razor-thin margins. Now they make money selling high-capacity enterprise drives to Amazon, Google, and Microsoft for AI infrastructure at premium prices with massive margins. Consumer products became the side business. Data centers became the main event.

Margin Expansion:

Cycle bottom: 22% gross margins

Current: Over 40% gross margins

The company Western Digital acquired in 2016 as a complementary flash business had transformed into something else entirely: a critical infrastructure play for the AI revolution.

Part Three: Three Immigrants, One Impossible Idea

The story of SanDisk begins with a failure.

Eli Harari, an Israeli-American engineer born in Tel Aviv in 1945, had already started one company and watched it die. Wafer Scale Integration (WSI), founded in 1983, collapsed despite Harari’s pioneering work on the technology that would become the foundation of flash memory. The experience scarred him. It made him careful about making the same mistakes twice.

At Hughes Aircraft in the 1970s, Harari had invented the Floating Gate EEPROM, the fundamental technology that makes flash memory possible. The innovation earned him recognition, but building a business around it proved elusive. When WSI failed, his wife Britt convinced him to stop chasing consumer gadgets and focus on what he actually knew: semiconductors.

In 1988, Harari connected with two other immigrant engineers.

Sanjay Mehrotra, an Indian-American who had overcome two visa rejections to study at UC Berkeley, was working at Intel and held over 70 patents.

Jack Yuan, a Taiwanese-American from Hughes Aircraft, provided complementary expertise in memory design.

“What happens when one Indian, one Chinese, and one person from Israel meet?” Mehrotra later asked.

The answer: they founded SunDisk in a small office in Palo Alto, California.

Their thesis was radical. They believed semiconductor-based flash memory would eventually replace magnetic storage—hard drives, floppy disks, even photographic film—for portable, battery-operated devices.

In 1988, this idea bordered on science fiction. Digital cameras barely existed. Mobile phones couldn’t store data. Flash memory was slow, unreliable, expensive, and dismissed by Intel and other major companies.

The founding insight was architectural. While the underlying flash memory chips had fundamental limitations, they wore out after repeated writes, they were slow, they lost data, Harari believed that sophisticated controller chips could manage these problems. The concept was called “System Flash,” pairing dumb memory with smart controllers that handled wear leveling, error correction, and garbage collection.

Early investors included U.S. Venture Partners and Matrix Partners. The company started with three employees and a vision for a market that didn’t exist.

The Early Years: Survival Through Rejection

The early years tested whether SanDisk’s thesis could survive contact with reality.

In 1991, SanDisk created its first commercial product: a 20-megabyte solid-state drive for IBM. The price: approximately $1,000. That’s $50 per megabyte. At those economics, flash memory was a niche curiosity, not a mass-market revolution.

The engineers spent two decades driving that cost down by more than 100,000 times through relentless innovation. Multi-Level Cell technology, a SanDisk invention, allowed each transistor to store multiple bits instead of just one. This effectively multiplied storage density without proportional cost increases.

But the company nearly didn’t survive long enough to benefit.

In 1988, Harari approached Kodak, which then controlled 70% of the world film market, with a proposition. SanDisk would develop removable flash memory cards as “digital film” for cameras. Kodak offered to fund the development but demanded something in return: a three-year exclusive on the technology.

Harari’s decision changed history. He rejected Kodak’s offer.

“In principle, I don’t like exclusivity. I like market forces working—competition,” Harari explained later.

This was a desperate startup turning down certain funding in favor of a theoretical competitive market. It was either brilliant or suicidal.

A decade later, Kodak held just 2% of the digital storage market while SanDisk held 50%. The decision to bet on open competition rather than guaranteed income from one customer created the conditions for SanDisk to become the dominant player.

Kodak, famously, went bankrupt.

The Samsung patent war of 1997 provided another existential test. When Samsung began using SanDisk’s MLC patents without licensing, SanDisk sued and took the case to the International Trade Commission. SanDisk won. Samsung products were barred from being shipped into the U.S. in 1997. Samsung signed a substantial five-year licensing deal. For a startup at that time, the $10 million Intel license for the same patents “was meaningful,” Mehrotra recalled. The victory validated that SanDisk’s intellectual property strategy wasn’t just defensive, it was a revenue generator.

Part Four: The Billion-Dollar Moat

SanDisk’s most consequential decision was a handshake in Japan in 1997.

Building a flash memory fab costs $10-20 billion. For SanDisk, constructing their own manufacturing was impossible. They didn’t have the capital. They couldn’t compete with Samsung’s massive investments.

So they formed a joint venture with Toshiba, the Japanese company that had invented NAND flash memory in 1987.

Toshiba contributed manufacturing technology and access to their Yokkaichi fabrication facility. SanDisk contributed Multi-Level Cell technology and controller expertise. Both invested jointly and shared R&D costs equally. Each marketed their share of output separately, competing in end markets while collaborating on manufacturing.

The partnership that changed everything:

Duration: 28 years and counting

Global production share: Roughly one-third of worldwide NAND

Manufacturing scale: World’s largest flash memory site (Yokkaichi)

Government backing: Billions in Japanese subsidies

What it survived: Toshiba spin-off, Kioxia rebranding, IPO, WD acquisition, SanDisk spin-off

The partnership outlasted everything because the economic logic remains unassailable: shared costs mean neither party bears the full burden of brutal capital requirements.

This is how a relatively small American company competed against Samsung’s tens of billions in factory investments. They didn’t try to match Samsung’s scale. They partnered with someone who could, then split the bill.

When the AI memory shortage hit in 2025, SanDisk had manufacturing capacity that most competitors couldn’t access. Not because they built it alone, but because they’d spent 28 years building a partnership that survived everything.

Part Five: The Milestones That Compounded

1995 - The IPO: The company renamed from SunDisk to SanDisk and went public under ticker SNDK at $10 per share. The capital fueled expansion exactly when digital cameras started mattering.

1994 - CompactFlash: Revolutionized digital photography. Photographers could swap cards in seconds, shooting hundreds of images without changing film. The format became the industry standard.

1999 - SD Cards: Rather than hoarding technology, SanDisk built open standards with Toshiba and Panasonic, licensing them broadly. This expanded markets faster than any single company could have captured alone.

2003 - $1 Billion Revenue & MicroSD: The tiny memory cards launched with Motorola would eventually power billions of smartphones.

2006 - M-Systems Acquisition: SanDisk paid $1.55 billion to acquire the Israeli company that invented USB flash drives. Suddenly SanDisk owned the technology behind thumb drives that replaced floppy disks.

2010 - Founder Transition: Eli Harari retired and Sanjay Mehrotra became CEO. One founder handing to another founder. The continuity mattered.

2016 - Western Digital Acquisition: SanDisk lost independence for nine years in a $16 billion deal. The marriage was always awkward, two companies with different cultures, different customers, different growth trajectories.

2025 - Independence Restored: The February spin-off freed SanDisk to pursue flash opportunities without compromise.

Every milestone built on what came before. The IPO funded CompactFlash. CompactFlash created cash flow for SD cards. SD cards funded USB drives. USB drives funded enterprise SSDs. Enterprise SSDs positioned the company for AI infrastructure.

Part Six: The Transformation

Most people think SanDisk makes memory cards. That’s like saying Amazon sells books. Technically true, but it misses everything.

What SanDisk was vs. what it became:

Consumer Products (now 15% of revenue):

SD cards for cameras

MicroSD cards for phones

USB drives

Enterprise Products (now 55% of revenue):

Data center drives

Server storage

Cloud infrastructure

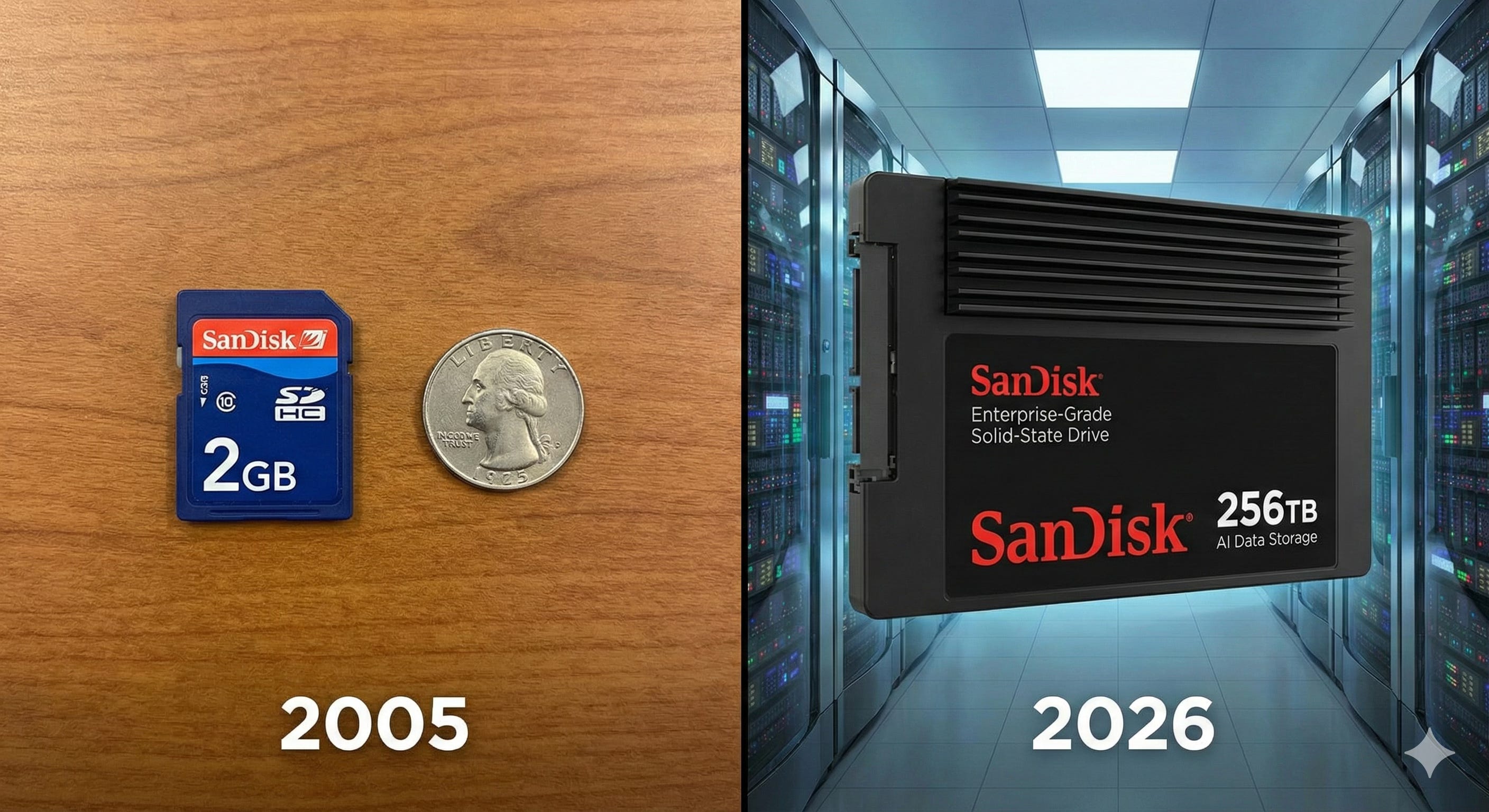

The 256-terabyte enterprise drive (highest-capacity drive ever shown)

The 256TB drive isn’t something you buy at Best Buy. It’s designed specifically for AI workloads, storing context windows that allow models to remember conversations, holding training data, providing fast access to massive datasets.

These are sold to Amazon, Google, Microsoft. Procurement teams placing orders for thousands of drives with multi-year delivery schedules.

The real money flows from AI infrastructure. The flash storage that remembers your ChatGPT conversation. The drives holding training data for new models. The memory enabling instant image generation.

This is what a memory card company became when it positioned for a transformation nobody predicted.

Part Seven: The Battlefield

The NAND flash market is an oligopoly. Five companies control 91% of global revenue.

Samsung (33% share): They make everything themselves, from the chips to the final product. They are the biggest player by far. But being that big makes it hard to change direction quickly when the market shifts.

SK Hynix (21-22% share): Became number two by acquiring Intel’s entire NAND business for $9 billion in March 2025. Also leads in HBM, giving leverage with AI chip customers.

Kioxia (12-17% share): SanDisk’s manufacturing partner through the 28-year-old joint venture. Combined with SanDisk, they represent 24-28% of the market.

Micron (11-13% share): Only U.S.-based pure-play memory maker, investing $125 billion in U.S. megafabs with CHIPS Act support. Competitive technology, but lacks partnership advantages.

SanDisk (10-12% share): Rapidly growing in enterprise. The only major player whose primary identity is flash memory for AI infrastructure.

Intel: Exited completely. One of flash memory’s inventors left the market because they couldn’t compete profitably.

SanDisk’s advantages come from positioning, not raw scale. The Kioxia partnership provides cutting-edge manufacturing without full capital costs. Products like the 256TB drive are purpose-built for workloads that didn’t exist five years ago. But Samsung’s scale enables larger R&D budgets, and the Kioxia partnership remains both advantage and existential risk.

What 38 Years Teaches

Lesson 1: Learn from failure, then go again. Previous failure is often the best teacher for future success, providing the necessary paranoia and discipline that first-time founders often lack. Eli Harari’s first startup, Wafer Scale Integration, collapsed despite having pioneering technology, and that specific failure instilled the discipline around focus and cash preservation that allowed SanDisk to survive for 38 years.

Lesson 2: Reject bad deals, even when desperate. Short-term certainty often comes with long-term constraints that kill the optionality needed to build large markets. SanDisk rejected Kodak’s offer for exclusive funding despite a desperate need for capital, a decision that allowed them to capture 50% of the digital storage market a decade later while Kodak held just 2%.

Lesson 3: Strategic partnerships can level the playing field. Building massive manufacturing infrastructure costs too much for most companies to do alone, but partnering allows you to split the bill while staying independent. SanDisk could not afford $20 billion fabrication plants to compete with Samsung, so they split the cost with Toshiba to build the world’s largest flash memory site, securing capacity they could never have built on their own.

Lesson 4: Patents can be a business model, not just defense. Intellectual property should not just be a legal shield; it can be a high-margin product that funds operations when product sales are tight. SanDisk sued Samsung for infringement and won an ITC ruling that barred Samsung products, forcing a licensing deal that generated critical revenue to keep the lights on when product margins were razor-thin.

Lesson 5: Create standards, not monopolies. Owning a small piece of a massive market is often more valuable than owning all of a tiny one. SanDisk chose to license its CompactFlash and SD card technologies to competitors like Toshiba and Panasonic rather than hoarding them, creating global standards that expanded the total market size faster than a closed ecosystem ever could.

Lesson 6: Survive downturns to capitalize on the recovery. Brutal market cycles wipe out weaker players, leaving the survivors with less competition and higher pricing power when demand returns. SanDisk endured the 2023 memory crash that wiped out 66% of industry revenue, which positioned them to enter the 2025 AI boom with the inventory and pricing leverage to drive a 559% stock surge.

The Verdict

SanDisk survived 38 years through a series of transformations that would have killed most companies. The digital film nobody wanted became memory cards that revolutionized photography, which became USB drives that replaced floppy disks, which became enterprise SSDs powering cloud infrastructure, which became AI storage enabling the current boom. Each transformation required abandoning what worked to build capabilities for markets that didn’t yet exist.

Independent for the first time in a decade, led by management who chose flash over hard drives, riding unprecedented memory demand while generating margins that seemed impossible two years ago. The company Eli Harari founded in 1988 bears little resemblance to what David Goeckeler leads in 2026, and that’s exactly why it survived.

But memory cycles always turn. Supply eventually catches demand, new capacity comes online, and pricing power evaporates. The companies that endure understand this reality. They save cash for the bad times. They use partnerships to share the heavy costs. They don’t just guess the future; they build flexible products that work no matter what happens next.

The memory card company everyone knew became the AI infrastructure play nobody expected. The transformation didn’t happen overnight. SanDisk spent years building enterprise relationships, qualifying products with hyperscalers, developing high-capacity drives without knowing exactly why those capabilities would matter. When AI memory demand exploded, they were ready not because they had a crystal ball, but because they had built a position that would win in many different scenarios.

What capability are you building today that might position you for a transformation you can’t yet see?

If you enjoy these breakdowns, share this article or subscribe for the next one.